How do I prioritize my financial needs and wants?

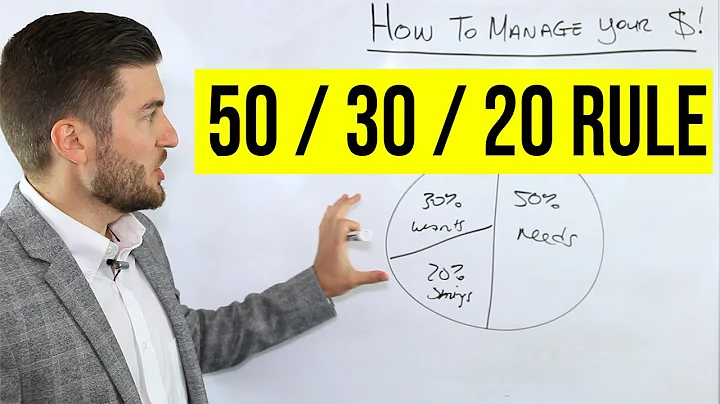

At NerdWallet, we recommend the 50/30/20 budget. If you distribute your monthly income in this fashion, you would spend 50% on needs, 30% on wants and 20% on savings and paying off debt. Plug your monthly take-home income into this budget calculator to determine how much you have available for each category.

Needs should be included in your budget first. Then, you'll have a sense of how much spending room you have for wants. You might also free up more money to put towards savings. Your needs and wants can change over time.

One popular budgeting method is the 50/30/20 budget rule. Under this method, you budget 50% of your income for needs, 30% for wants, and 20% for savings or debt repayment. This is a great starting point for creating a budget, but you may need to adjust the percentages depending on your specific situation.

Key short-term goals include setting a budget, reducing debt, and starting an emergency fund. Medium-term goals should include key insurance policies, while long-term goals need to be focused on retirement.

The 50-30-20 rule recommends putting 50% of your money toward needs, 30% toward wants, and 20% toward savings. The savings category also includes money you will need to realize your future goals. Let's take a closer look at each category.

The four primary financial objectives of firms are; stability, liquidity, profitability, and efficiency. The profitability objective focuses on generating enough revenue to meet the firms' expenses and the desired profit margin.

Needs are essential items that you require to survive and thrive, while wants are things that you desire but can do without. The impact of needs versus wants on your budget can be significant and it is important to prioritise your needs over your wants to avoid overspending and falling into debt.

Needs are considered as the basic items essential for human survival. Food, water, and shelter are examples of needs. Wants are anything that we desire or would like to have. Wants can be for entertainment purposes, or tools that make our lives easier.

A need is something that is necessary to live and function. A want is something that can improve your quality of life. Using these criteria, a need includes food, clothing, shelter and medical care, while wants include everything else.

That's why it's important to set SMART financial goals – goals that are Specific, Measurable, Achievable, Relevant and Timely. Setting specific and measurable financial goals makes it easier for you to track your progress and take corrective steps when necessary.

How to budget $5,000 a month?

Consider an individual who takes home $5,000 a month. Applying the 50/30/20 rule would give them a monthly budget of: 50% for mandatory expenses = $2,500. 20% to savings and debt repayment = $1,000.

Personal finance expert Dave Ramsey says if you're going through a tough financial period, you should budget for the “Four Walls” first above anything else. In a series of tweets, Ramsey suggested budgeting for food, utilities, shelter and transportation — in that specific order.

Are you approaching 30? How much money do you have saved? According to CNN Money, someone between the ages of 25 and 30, who makes around $40,000 a year, should have at least $4,000 saved.

Life goals are all the things you want to accomplish in your life. Often your life goals are very meaningful to you and can make a lasting impact on your life. They can be large and challenging goals, or they can be smaller and more personal. It all depends on what you want to achieve.

A financial goal is a target set when you manage your money and make financial decisions. It can involve saving plans, spending limits, earning, or even investing. Creating a list of financial goals is vital to creating a budget.

Whether you're saving for emergencies, paying off debt, or building retirement savings, all financial goals can be considered needs. Achieving your Money Milestone is essential to staying financially fit and takes precedence over your wants throughout your journey to Financial Freedom.

We all have needs, not just for basic survival, but 6 profound needs that must be fulfilled for a life of quality. The needs are: Love/Connection, Variety, Significance, Certainty, Growth, and Contribution. The first four needs are necessary for survival and a successful life.

Food, water, clothing, and shelter are all needs. If a human body does not have those things, the body cannot function and will die. Wants are things that a person would like to have but are not needed for survival. A want may include a toy, expensive shoes, or the most recent electronics.

One way to prioritize is the “Five Fs”: faith, family, friends, fitness, and finances. This model allows you to create a system that ensures you remain true to your values while reaching for professional success. As individuals, we are saddled with numerous responsibilities and goals.

The Fundamentals of Problem Prioritization

Take the time to understand the issue at hand, its underlying causes, and the desired outcome. A clear problem statement will help you determine whether it should be given immediate attention or if it can be addressed later.

How do you prioritize what should be done first?

First, focus on getting things done that are both important and urgent. Then, move on to things that are important but not urgent. Regularly review and adjust your priorities to reflect changes in deadlines or project directions.

The difference between needs and wants is crucial for effective financial management. Needs are the essential items or services necessary for a comfortable life, such as food, shelter, and healthcare. Wants, on the other hand, represent desires or non-essential expenses, like luxury items or unnecessary subscriptions.

Our needs are the things we must have to sustain us day to day: food, shelter, clothing, personal care items, and in most cases safe, reliable transportation. Just about everything else can be classified as a want – entertainment, electronics, leisure travel … the list of things we want is potentially endless.

Balancing our wants and needs is important for several reasons: Financial stability: Balancing wants and needs helps to ensure that we live within our means and avoid overspending on things that we don't actually need. This can lead to financial stability and reduce the risk of debt and financial difficulties.

Understanding how to create a realistic budget, track your spending, and set attainable savings goals are essential steps in the process. It can be overwhelming to take on all these tasks at once, but when broken down into smaller steps, money management success is achievable.